Rishi Sunak has delivered a Budget which set out billions of extra spending to help the economy through the coronavirus crisis – but then massive tax hikes to pay for it.

Here are some of the key questions:

What has he announced?

Although the Budget speech had been extensively briefed in advance, the scale of the emergency support on offer to the economy is staggering – £65 billion extra over the course of this year and next, a total of £407 billion since the crisis began.

Measures announced include the extension of the furlough scheme, the £20 a week Universal Credit increase and the business rates holiday.

The housing market will be supported by an extension of the stamp duty cut and a new mortgage guarantee.

Why is he doing this?

In short, because the economy has been devastated by the impact of the virus and the lockdowns put in place to control it and still needs a financial lifeline.

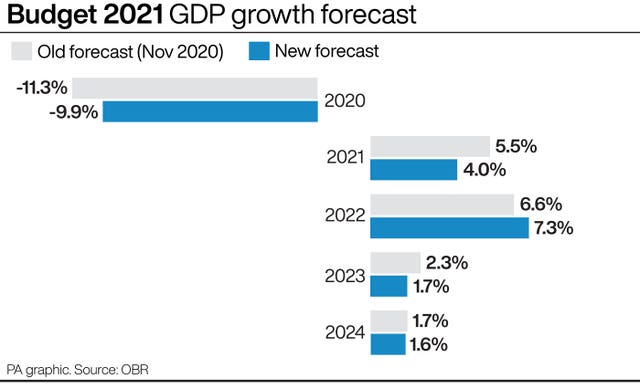

Although the recovery is expected to be “swifter and more sustained” than the Office for Budget Responsibility (OBR) had forecast in November – largely as a result of the vaccine programme – there will still be long-term damage.

The OBR expects the economy to return to its pre-Covid level by the middle of next year – six months earlier than previously thought – but in five years’ time it will still be around 3% smaller than it would have been if the pandemic had not struck.

What has this done to the nation’s finances?

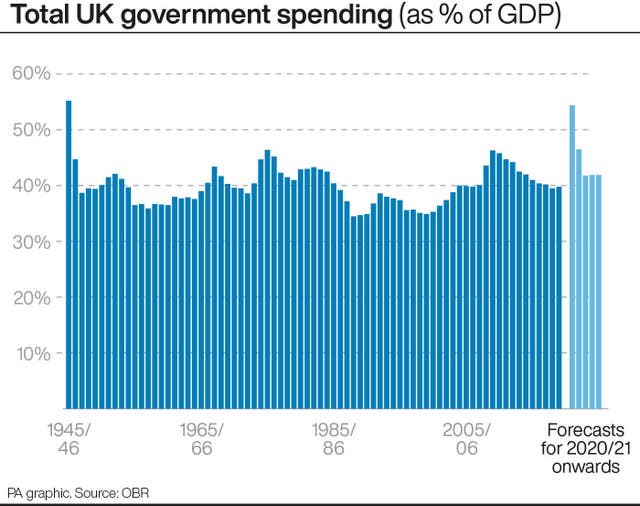

The OBR predicts Government borrowing will soar to £355 billion in 2020/21 – lower than the £394 billion first forecast but still 17% of national income and the highest level since the Second World War.

Borrowing will remain at eye-watering levels in 2021/22 at £234 billion, up from the £164.2 billion pencilled in before and 10.3% of GDP, but will fall gradually to 2.8% in 2025/26.

How is all this going to be paid for?

In the short term, it will not be, partly because the economy still needs support and partly because borrowing is still relatively cheap for the Government.

But Mr Sunak set out plans to increase corporation tax and rake in more money from income tax over the coming years as he sets the nation’s finances on a path to sustainability.

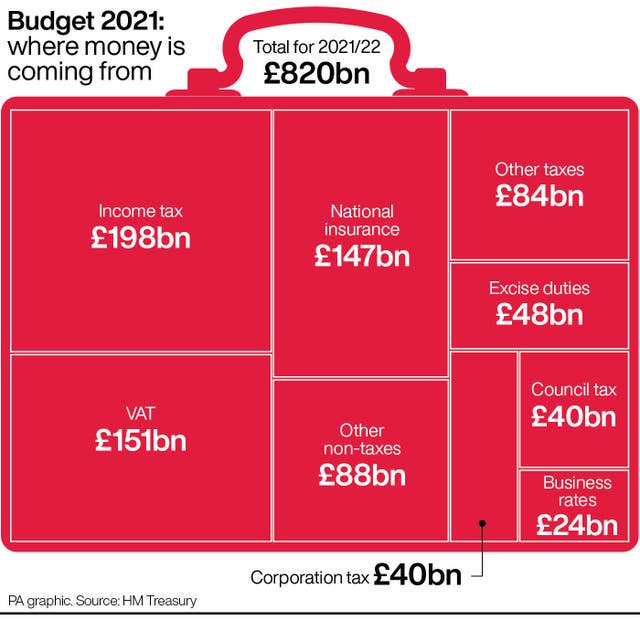

Corporation tax will increase from 19% to 25% in 2023, although smaller firms will pay lower rates, taking in an extra £17.2 billion in 2025-26.

Income tax thresholds will be frozen from April this year, which will mean more people paying tax – or a higher rate – as wages increase over time, resulting in an extra £8.18 billion for the Exchequer in 2025-26.

The OBR said the tax rises set out in the Budget increase the overall tax burden to its highest level since the late 1960s.

What has the Chancellor said about his plan?

He told MPs: “These are significant decisions to have taken. Decisions no Chancellor wants to make.

“I recognise they might not be popular. But they are honest.”

What has the reaction been?

Tony Danker, director-general of the Confederation of British Industry, said that while the Budget protects the economy and will help kickstart the recovery “it leaves open the question of UK competitiveness long term”, with the corporation tax hike causing “a sharp intake of breath for many businesses”.

Labour leader Sir Keir Starmer said: “This is a Budget that didn’t even attempt to rebuild the foundations of our economy or to secure the country’s long-term prosperity. Instead, it did the job the Chancellor always intended, a quick fix, papering over the cracks.”

Comments: Our rules

We want our comments to be a lively and valuable part of our community - a place where readers can debate and engage with the most important local issues. The ability to comment on our stories is a privilege, not a right, however, and that privilege may be withdrawn if it is abused or misused.

Please report any comments that break our rules.

Read the rules hereLast Updated:

Report this comment Cancel