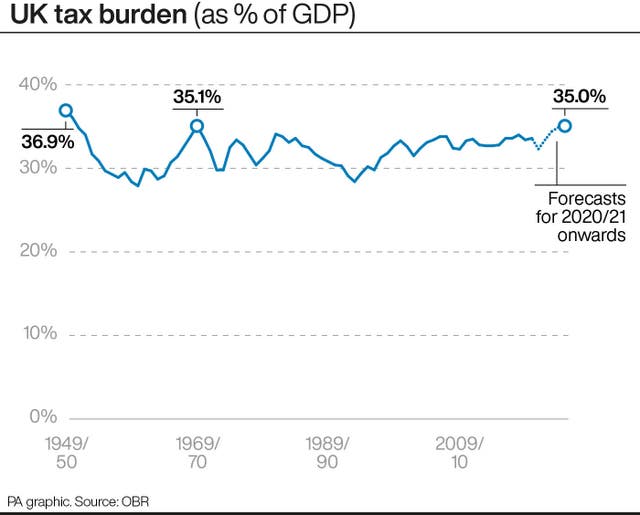

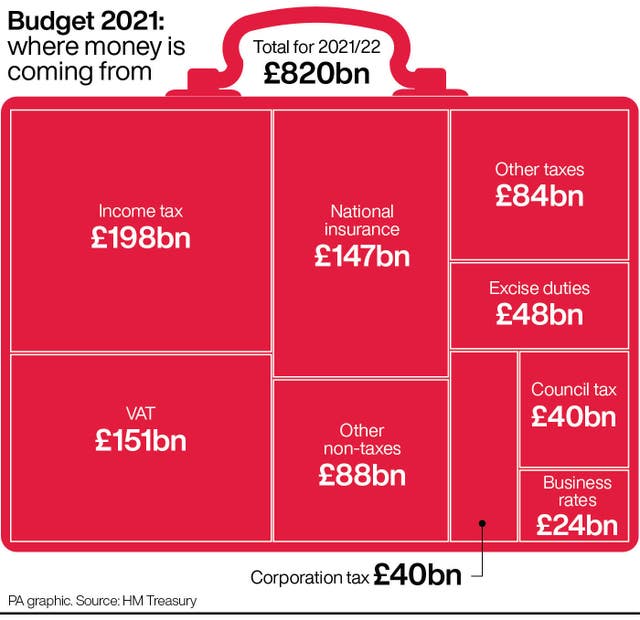

British households and businesses will shoulder the biggest tax burden since the 1960s after Rishi Sunak set out plans to begin repairing the nation’s finances after the coronavirus crisis.

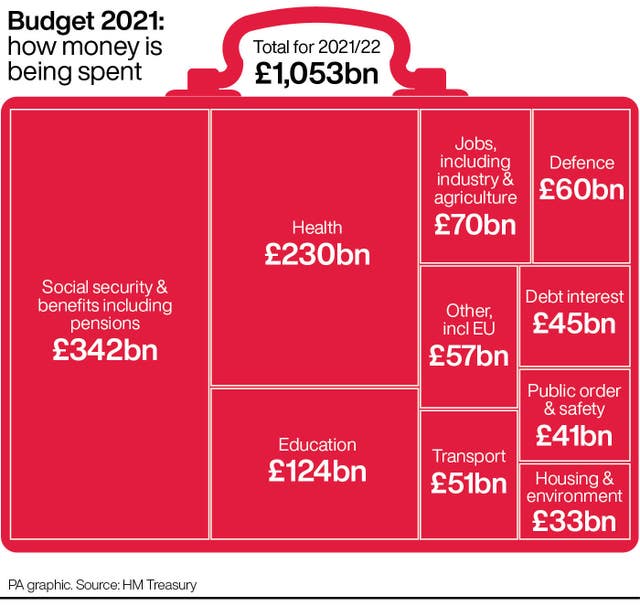

The Chancellor used his Budget to extend the furlough scheme and Universal Credit increase as part of a £65 billion lifeline for an economy still battered by the pandemic.

But taxes on business profits are set to be hiked from 2023, while income tax thresholds will be frozen, meaning more than a million extra people will be dragged into paying it as wages increase.

The Office for Budget Responsibility (OBR) said increasing the headline corporation tax rate, freezing personal tax allowances and thresholds, and cuts of around £4 billion from departmental spending plans would raise a total of £31.8 billion in 2025-26.

The measures increase the tax burden from 34% to 35% of gross domestic product (GDP) – a measure of the size of the economy – in 2025-26, “its highest level since Roy Jenkins was chancellor in the late 1960s”.

Analysts expect the tax hikes to help eliminate the current budget deficit in 2025-26, meaning the Government is not borrowing to fund day-to-day spending.

Mr Sunak told MPs: “These are significant decisions to have taken. Decisions no Chancellor wants to make.

“I recognise they might not be popular. But they are honest.”

He said the total package of measures to support the economy – including those already announced – amounted to £407 billion, but warned the unprecedented spending could not continue.

The point at which people begin paying income tax will increase by £70 to £12,570 in April, but will be maintained at that level until April 2026, meaning more people will be dragged into paying tax as wages increase.

The 40p rate threshold will increase by £270 to £50,270 and then be frozen, with the measures raking in almost £8.2 billion in 2025-26.

The Institute for Fiscal Studies (IFS) said about 1.3 million people would be brought into the income tax system, with about 10% of adults brought into the higher 40p rate.

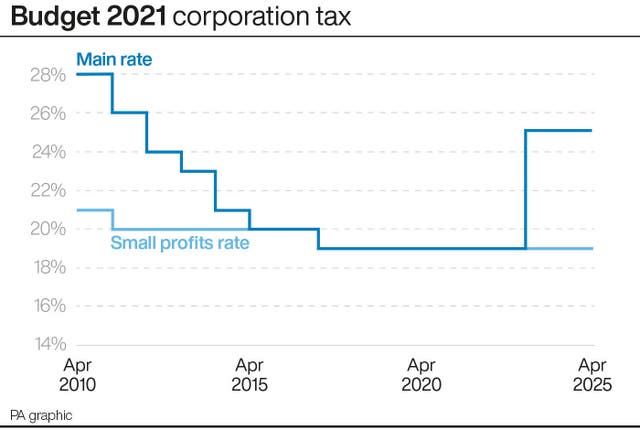

Corporation tax will increase from 19% to 25% in 2023, raising £17.2 billion in 2025-26, although only firms with profits of £250,000 or more will pay the full rate.

There will be a “super deduction” for companies when they invest, reducing their tax bill by 130% of the cost.

Mr Sunak insisted the UK would still have the lowest effective corporation tax rate in the G7 group of industrialised economies.

At a Downing Street press conference he defended the increase in the tax burden, saying: “I don’t think any other chancellors have had to do as much fiscal support for the country as I’ve had to.”

Confederation of British Industry director-general Tony Danker said the move would “cause a sharp intake of breath for many businesses and sends a worrying signal to those planning to invest in the UK”, although he welcomed measures to protect the economy now and kickstart the recovery.

While economists have largely agreed that immediate measures to repair the nation’s finances are not needed while the impact of the coronavirus crisis is still being felt, the need for medium-term action was underlined by the OBR forecasts.

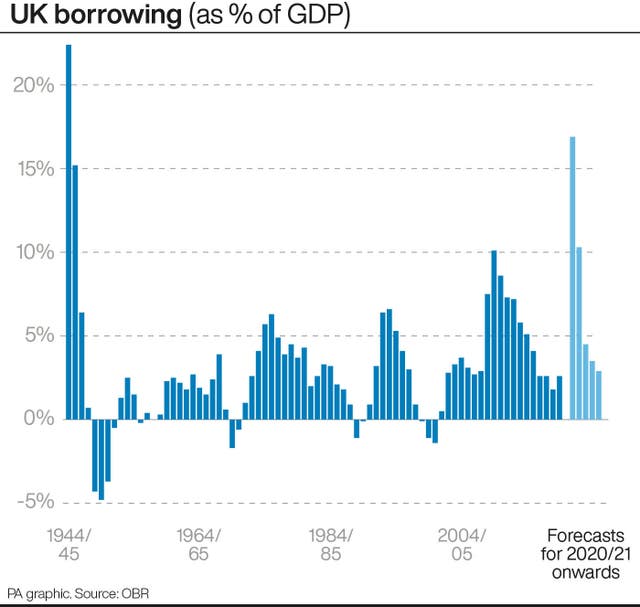

Mr Sunak said borrowing this year was £355 billion, 17% of national income – the highest level since the Second World War – while next year it is forecast to be £234 billion, 10.3% of GDP.

He added: “Without corrective action, borrowing would continue at very high levels, leaving underlying debt rising indefinitely.”

The Budget measures will see borrowing fall to 4.5% of GDP in 2022-23, 3.5% in 2023-24, then 2.9% and 2.8% in the following two years.

The underlying national debt, excluding the Bank of England, will peak at 97.1% of GDP in 2023-24, the OBR said.

The OBR expects the economy to return to its pre-Covid level by the middle of next year, six months earlier than previously forecast as part of a “swifter and more sustained” recovery, largely as a result of the vaccine rollout.

But in five years the economy will still be 3% smaller than it would have been if the pandemic had not struck.

Growth next year is expected to be 7.3%, up from 6.6%, but the OBR cut its GDP forecast for every other year until 2025, including a cut for this year to 4% from the 5.5% growth previously expected.

Unemployment caused by the pandemic is forecast to be lower than expected, peaking at 6.5%, down from 11.9% predicted last July.

The Chancellor also:

– Extended the stamp duty holiday for properties less than £500,000 until the end of June, then a new £250,000 threshold will apply until the end of September before returning to £125,000.

– Confirmed the furlough scheme will run until the end of September, although employers will be expected to make a contribution from July.

– Extended the 5% reduced rate of VAT for the tourism and hospitality sector to the end of September, with an interim rate of 12.5% for another six months after that.

– Continued the business rates holiday for the retail, hospitality and leisure sectors until the end of June, with a discount applying for the rest of the financial year.

– Announced the temporary £20-a-week increase in Universal Credit payments will continue for a further six months.

– Set out a new Recovery Loan Scheme to replace previous coronavirus loan packages, allowing businesses of any size to apply for loans from £25,000 up to £10 million through to the end of the year, with the Government providing lenders with an 80% guarantee.

– Froze alcohol duties and scrapped a planned increase in fuel duty.

– Announced eight new freeports in England and a new “economic campus” for the Treasury and other Whitehall departments in Darlington.

Paul Johnson, director of the Institute for Fiscal Studies think tank, said “we are in a new phase of UK economic history” and “taxes (are) likely to be at their highest sustained level”.

Labour leader Sir Keir Starmer said the Budget was a “quick fix, papering over the cracks” which “didn’t even attempt to rebuild the foundations of our economy or to secure the country’s long-term prosperity”.

Comments: Our rules

We want our comments to be a lively and valuable part of our community - a place where readers can debate and engage with the most important local issues. The ability to comment on our stories is a privilege, not a right, however, and that privilege may be withdrawn if it is abused or misused.

Please report any comments that break our rules.

Read the rules here